FINNISH ECONOMY 2017/2

The global economy is experiencing an upswing, even though production growth has not reached pre-financial crisis levels. GDP is estimated to grow in the United States by over 2 per cent annually during 2017-2019. The growth will be driven by domestic demand, which may be strengthened by the fiscal policy of the new government in the coming years. The growth rate will be slightly faster than the growth of potential output, leading to the acceleration of inflation and a rise in interest rates. The policies of the new president are a major source of uncertainty, especially regarding fiscal and trade policy.

The GDP of the EU area will grow by 2.1 per cent this year, 1.8 per cent in 2018 and 1.6 per cent in 2019. Growth will be clearly faster this year than previously expected, although anticipation of Brexit is hampering Britain’s growth. In Europe, growth is also slightly faster than potential output growth. High unemployment will nevertheless dampen the acceleration of inflation. In Russia, GDP will increase by about one and a half per cent annually between 2017 and 2019, as energy prices are no longer decreasing. In the longer term, however, a pick-up in economic growth will require the acceleration of reforms. China’s GDP will increase by 6.7 per cent this year, which is more than forecast in the spring. Efforts to curb heavily increased indebtedness and shifting from an export industry to services will slow down production growth over the next few years. Growth will slow down in 2018 to 6.5 per cent and next year it will be closer to 6 per cent.

Between 2017 and 2018, global GDP growth will accelerate to 3.5 per cent, but it will slow down somewhat in 2019. Growth in so-called emerging economies is curbed by the slowdown in China’s growth. Countries producing raw materials will benefit from the moderate rise in raw material prices over the next few years.

A risk of less favourable development than forecast still exists. Recently, President Trump’s protectionist speeches have aroused concern. As the level of public debt in many euro area countries is high and banks’ capital adequacy is rather weak, the possibility of financial market crises still exists. In China, the biggest problem is the high debt level of the corporate sector, which could under conditions of weak economic growth spur difficulties in debt servicing.

Eastern Ukraine is bogged down in a frozen conflict. Old Russian sanctions will not be lifted in the near future and new ones will be introduced. The political crisis will hamper economic relations between Russia and Western countries for several years. Uncertainty is also being spawned by the war still going on in Syria and Iraq, as well as threats relating to North Korea’s nuclear armament and possible countermeasures.

In 2016, euro area GDP grew by 1.8 per cent. GDP growth towards the end of last year accelerated compared to the previous quarter in the region and was 0.6 per cent in the second quarter of 2017. Leading indicators suggest that the trend has continued in the third quarter of this year. Future growth will hinge closely on the development of business and household confidence. Low interest rates and the continuing low prices of oil support the growth of energy-intensive euro economies. The recent strengthening of the euro’s exchange rate will curb their exports somewhat.

We forecast euro area GDP will increase by 2.1 per cent in 2017 and by 1.8 per cent in 2018. Growth will decelerate to 1.6 per cent in 2019.

There will continue to be differences in growth between the euro economies in the next few years. In 2017 GDP growth is 4 per cent in Ireland, 3 per cent in Spain, 2.5 per cent in the Netherlands, 2 per cent in Germany and Greece, and about 1.5 per cent in France and Italy. Their current accounts will strengthen and growth of public debt will slow down, although not very quickly. The large public debt makes the economy of many euro countries vulnerable.

Monetary policy in the euro area is very loose, and we expect it to normalize slowly. We estimate that the ECB will start reducing the amount of securities purchases in the beginning of 2018, but the raising of interest rates will have to wait until the beginning of 2019.

The immediate effect of the ECB’s loose monetary policy is that interest rates will remain low and the euro exchange rate will be weaker than it would otherwise be. Low interest rates and high liquidity support the rise in equity prices. In some countries, the loose monetary policy may bring about an unhealthy increase in housing prices.

Strengthening of the euro area crisis management mechanisms, in tandem with the ECB’s loose monetary policy and the accelerated economic growth, has calmed the region’s financial markets. However, there is still a risk of crises, as public debt is high in many countries and there are several banks exhibiting low solvency ratios in the region (especially in Italy). There is also a threat of a new crisis in Greece.

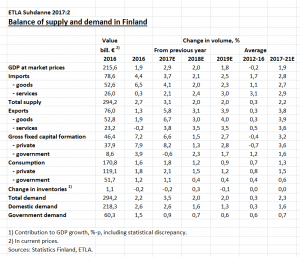

According to preliminary data from the National Accounts, Finland’s GDP grew by 3.1 per cent in the first half of 2017 compared to last year’s figures. The volume of total exports increased by nearly 10 per cent. There were significant increases in exports to several regions, including Russia. Private consumption increased by two per cent. Consumption was bolstered by low inflation, moderate employment improvement, a rise in unearned income as well as strong consumer confidence. Investment experienced a sharp increase.

Finland’s GDP will grow by 2.9 per cent in 2017, 2.0 per cent in 2018 and 1.8 per cent in 2019.

Finland’s GDP is estimated to increase by 2.9 per cent in 2017. In March, we predicted an increase of 1.7 per cent. This upward revision is mainly due to growth being faster than expected in the first half of this year, resulting from a strong increase in investment, private consumption, and exports. Euro area growth forecasts have also been increased considerably. Exports will grow strongly this year. Investment will increase only slightly less than last year. Private consumption will grow by a couple of per cent, fueled by higher employment and a low savings rate, even though real incomes will decline slightly from last year. In 2018, GDP will increase by 2.0 per cent. Export growth will slow down due to the decline of ship deliveries. Investment growth will also subside considerably as major projects are completed. Private consumption will increase somewhat less than this year. In 2019, GDP will increase by 1.8 per cent, which is still somewhat faster than growth of production potential. Growth is driven by exports and investments, in particular.

The volume of exports will increase in 2017 by almost 6 per cent. Exports of goods will increase by almost 7 per cent while service exports climb by almost 4 per cent. Exports are fostered by the gradual recovery of investment in export countries, competitiveness, boosted by the Competitiveness Pact and export industry capacity increasing through investments. Exports of motor vehicles will increase by more than a third due to the sizeable expansion of the new car plant in Uusikaupunki. Exports of other vehicles (mainly ships) will increase by 65 per cent. Exports of wood products will increase by 9 per cent. Electrical equipment manufacturing and electronics industry exports will increase by 8 per cent. Exports of paper and metal products will increase by two per cent. Exports to Russia will already achieve clear growth.

In 2018 the total export volume is projected to increase by about 3 per cent. Growth will slow down due to the decline in ship deliveries compared to this year. Exports are increasing in all other industries. Growth in the forest industry is particularly rapid owing to the new capacity of the Äänekoski biotechnology plant. Exports to Russia and other raw material-producing countries will strengthen if raw material prices develop as expected. The volume of exports will increase in 2019 by almost 4 per cent, boosted by the rather high amounts of ship deliveries. The fairly positive export development forecast is based on the assumption that cost competitiveness will continue to improve slightly over the next few years, which will require the continuation of wage moderation.

We forecast that investment will increase by about 6.5 per cent in 2017. Machinery and equipment investment will increase by 12 per cent fuelled by large investment projects. Residential housing construction will continue to grow rapidly at a rate of 6.5 per cent. Public investment will decline slightly as a result of the high level of comparison of last year brought about by large infrastructure projects.

In 2018 total investment growth will slow down to 1.5 per cent. Machinery and equipment investment will decrease by a couple of per cent due to the high level of comparison of this year. Growth in residential housing construction will slow down to about 1.5 per cent, but construction will continue at a high level. In 2019 the growth of total investment will climb above 2.5 per cent as the growth of companies’ machinery and equipment investment accelerates in the wake of nuclear power plant investment.

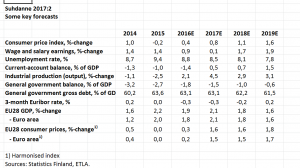

The recent strengthening of domestic demand has also boosted employment. The number of employed persons has increased from mid-2015 to mid-2017 by 47,000 persons and the seasonally adjusted employment rate has risen by 1.3 percentage points to 69.3 per cent. We forecast that this trend will continue, but the increase in employment from 2015 to 2019 will remain at 61,000 persons. The employment rate will rise to 70.5 per cent, which is clearly less than the government’s goal of 72 per cent. The unemployment rate will also decline, but less than could be expected based solely on employment developments, as the supply of labour is also increasing. For 2017 we forecast an 8.5 per cent unemployment rate. After this the unemployment rate will decrease by 0.3-0.4 percentage points per year. It will be 8.1 per cent in 2018 and 7.8 per cent in 2019. Improving exports will also boost employment in industry. Our forecast for the unemployment rate in 2021 is 7.2 per cent with an employment rate of 71.4 per cent.

In 2017 moderate wage agreements, increases in payroll taxes paid by employees in line with the Competitiveness Agreement, public sector holiday pay cuts together with accelerating inflation will result in a slight decline in real earnings. Rising employment and strong household confidence will nevertheless lead to a 2.1 per cent growth in private consumption. The savings rate will still decrease slightly.

In 2018 private consumption will increase by 1.5 per cent. The real disposable income of households will increase by the same amount due to the improvement of employment and rise of income. We have estimated a real income increase of 0.6 per cent. In 2019 private consumption will increase by 1.2 per cent, which will slightly surpass the increase in real disposable income due mostly to employment growth. If wage agreements are not moderate, the growth in consumption may be faster in the short term, but deteriorating employment in the long run will limit the growth of GDP and consumption.

Consumer prices are expected to rise by 0.8 per cent in 2017. Inflation is fueled by a slight increase in oil prices from last year. Consumer prices are projected to rise in 2018 by 1.1 per cent, due to price rises for example in housing, tobacco, alcohol, and services. In 2019, consumer prices will rise by 1.6 per cent. At this time, rising interest rates will contribute to the acceleration of inflation.

In 2016 the total public sector deficit was 1.8 per cent of GDP. The central government deficit was 2.7 per cent and the municipalities’ deficit was 0.4 per cent. The surplus of social security funds was a little over one per cent. We estimated that the so-called structural deficit of the public sector was 0.2 per cent in relation to GDP. The corresponding EMU norm is a maximum of 0.5 per cent, but it has its own adjustment mechanisms. Overall public gross debt was 63.1 per cent of GDP, which was 0.5 percentage points lower than in the previous year. The rise of the debt was curbed by a simultaneous decrease in the central government’s cash funds.

In 2017 the public sector deficit will be reduced to 1.5 per cent of GDP, fueled by rapid economic growth, in spite of the income tax cuts implemented. The government debt will stabilize to last year’s 63.1 per cent. Using the methodology of the EU Commission and calculated on the basis of the Etla’s forecast, the public sector structural deficit is projected to increase to 0.9 per cent of GDP in 2017 due to the narrowing of the so-called output gap.

In 2018 the public sector’s deficit will subside to 1.0 per cent as the government deficit decreases, due to adjustment measures and economic growth. The surplus of social security funds is gradually decreasing as pension expenditures increase. The public sector’s structural deficit is 0.6 per cent of GDP. The deficit will be decreased by a decline in the actual deficit, but the descent will be dampened by the narrowing of the output gap. The GDP ratio of public debt will fall to 62.2 per cent of GDP.

In 2019 the overall public deficit will continue to decline to 0.6 per cent of GDP. The central government deficit will be 1.3 per cent of GDP at that time. The GDP ratio of public debt will fall to 61.4 per cent of GDP. Keeping a tight rein on public sector spending and revenues will continue to be a prerequisite for the favourable growth.

Finland clearly meets the 3 per cent public sector deficit target. In 2021 the deficit will be 0.1 per cent of GDP, which means that the increase in public sector’s indebtedness will almost come to a halt. Accelerated economic growth has also considerably eased the fulfillment of the 60 per cent debt criterion. The debt will not grow as much as previously estimated in the spring and in 2018 the debt-to-GDP ratio will already be decreasing. The descent will continue so that in 2021 the debt will be 59.5 per cent of GDP. The development is nevertheless very sensitive to economic growth and the GDP deflator.

The structural deficit is still a problem for Finland with regards to the so-called preventive component of the EMU criterion. It is calculated from the actual public sector deficit by conducting a cyclical and structural correction to it. The key question in the calculation is how high Finland’s so-called potential output is estimated to be. The bigger the difference between the potential GDP and the actual GDP (the so-called output gap), the smaller the structural deficit is in relation to the actual deficit. When the output gap narrows, the structural and actual deficit are the same. We estimate that the structural deficit will exceed the medium-term target level in 2017 and 2018. However, as the deficit remains below 1 per cent (not significantly different) and clearly decreases, the structural deficit criterion will also be met.

The EMU norms still have an additional criterion, the so-called expenditure benchmark, according to which public spending should not grow faster than potential GDP. Interpretation of this indicator is still evolving. It also has problems regarding uncertainties surrounding the calculation of potential output.

Further information:

Markku Kotilainen

Research Director, Dr. Soc. Sc. (Econ.)

ETLA-Research Institute of the Finnish Economy

tel. +358-9-609 90 206

email:markku.kotilainen@etla.fi