ETLA SUHDANNE 2017/1

The world economy is undergoing an upswing, even if the growth rate of production does not meet pre-financial crisis levels. US gross domestic product is expected to grow by just over 2 per cent per annum during 2017 to 2019. The growth is driven by domestic demand, which the fiscal policy of the new government is likely to boost in the coming years. The rate of growth is slightly faster than the estimated growth of production potential, which will spur inflation and a rise in interest rates. The policies of the new president are a key uncertainty, especially regarding fiscal and trade policy.

The GDP of the total EU area will expand by 1.7 per cent this year, 1.6 per cent in 2018 and 1.5 per cent in 2019. Growth will be slightly faster in Europe than the growth of production potential. High levels of unemployment will nevertheless curb the acceleration of inflation. In Russia, GDP will grow by slightly over one percentage point in 2017. During 2018-2019 the growth rate will climb to about one and a half per cent. Rising energy prices will boost growth. In the long term, however, the acceleration of economic growth will require the hastening of reforms. China’s GDP will increase by 6.3 per cent this year, which is clearly less than previously. Attempts to rein in the strong growth of debt and the shift from the export industry to services is dampening the growth of production. Growth will slow to 6 per cent in 2018 and to slightly below this in 2019.

In 2017 global GDP growth will accelerate to 3.3 per cent, remaining at approximately the same level in the following years. Growth of the emerging economies will be curbed by the slowdown in China’s growth and weakening foreign capital inflows due to the anticipated tightening of monetary policy in the United States. Countries producing raw materials will benefit from the modest increase of commodity prices.

The risk of substantially less favourable development is still great. Recently, particular concern has been raised by the protectionist rhetoric of the new US president. Uncertainty is exacerbated in the euro area by the Dutch parliamentary elections in March, the French presidential elections in May and the German Bundestag elections in September. As the level of public debt is high in a number of euro area countries and the capital adequacy of banks weak, political instability could, at worst, trigger speculation about the future of the entire euro area. In China the biggest problem is the high level of debt within the business sector, which could create difficulties for debt management amidst weakening economic conditions.

Eastern Ukraine is bogged down in a frozen conflict. Sanctions will not be dismantled in the near future and the crisis will hold back economic relations between Russia and the West for several years. Uncertainty is also increased by the never-ending war in Syria and its neighbouring countries.

GDP in the euro area increased in 2016 by 1.7 per cent. Its GDP growth compared with the previous quarter remained stable in the second half of last year at 0.4 per cent. Growth in the fourth quarter was of the same magnitude in both Germany and France. In Italy growth was only 0.2 per cent. Indicators suggest that this trend will continue in January-February. The continuation of growth in the future depends crucially on the development of business and household confidence. Low interest rates and the still low level of oil prices will boost the growth of energy importing euro economies. The weaker euro exchange rate will strengthen their exports.

We forecast that euro area GDP will grow by 1.6 per cent in both 2017 and 2018. Growth will slow to 1.5 per cent in 2019.

There will continue to be differences in growth rates between euro economies in the next few years. In 2017 GDP growth will be 4 per cent in Ireland, 2.5 per cent in Spain, 2 per cent in the Netherlands, 1.7 per cent in Germany and 1.4 per cent in France. Italy is lagging behind at about one per cent, which is the lowest in the euro area, while even Greece reached one and a half per cent growth. The current account deficits continue to shrink and public debt growth will slow down, though not very fast. The high public debt makes the economy of many euro countries vulnerable.

On March 10 2016, the European Central Bank lowered its refinancing rate from 0.05 percent to 0.00 per cent. The bank overnight deposit rate was lowered from the previous -0.3 per cent to -0.4 per cent. In addition to its interest rate policy, the ECB carries out asset purchase programme designed to bolster aggregate demand and raise inflation closer to its target level. In December 2016 it was decided that purchases will continue at a rate of Eur. 80 billion a month until March 2017 and after this point Eur. 60 billion a month until December 2017. They can be continued after this point until the rate of inflation has been elevated permanently towards the ECB’s slightly less than 2 per cent inflation target.

The direct effect of the ECB’s easy monetary policy is that interest rates will remain low and the euro exchange rate will be weaker than it otherwise would be. The low level of interest rates and high liquidity are spurring a rise in stock prices. In some countries, the easy monetary policy may result in an unhealthy rise in housing prices.

Strengthening the euro area crisis management mechanisms, in conjunction with the ECB’s easy monetary policy, has managed to calm the areas financial markets. However, the risk of crises still exists, because public debt is high in many countries and the euro area (especially in Italy) has a number of banks with weak solvency. Typical new threats for the ongoing year are elections, where populist parties have the opportunity to succeed. This could, at worst, give rise to speculation on the break-up of the euro area. There is also a threat of a new crisis in Greece, because the political leadership is required to make difficult commitments to the ongoing implementation of the austerity programme. Greece’s economic situation is also undermined by the considerable influx of refugees via Greece to other EU countries.

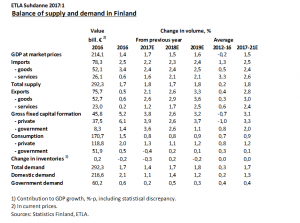

According to preliminary national accounts figures, Finland’s GDP grew by 1.4 per cent in 2016. The volume of exports grew only slightly. The decline of the value of Russian exports fell to six per cent. Private consumption increased by a few percentage points. Consumption was fuelled by low inflation, a slight improvement in employment and strong consumer confidence. Investment rose rapidly and in tandem with private consumption they were a key engine of growth. Consumer prices increased slightly.

Finland’s GDP is expected to grow by 1.7 per cent in 2017. In September 2016 we predicted 1.2 per cent growth. The upward revision is partly due to the so-called carry-over effect generated by the rapid growth in the second half of last year, which derives from the stronger investment than projected and the increase of private consumption. During the current year, exports will experience an upswing in growth to around two per cent. Investment will increase only slightly less than last year. Private consumption will increase by slightly over one per cent, boosted by better employment, although real earnings will remain at about last year’s level. In 2018, GDP will grow by 1.5 per cent. Export growth will become slightly stronger, while investment growth will slow down somewhat. Private consumption will grow slightly less than this year, but still over one per cent. In 2019 GDP will increase by 1.6 per cent. The composition of growth will be very similar to that of 2018.

The development of exports was still weak last year. The entire volume of exports increased by only 0.7 per cent in 2016. This was based almost entirely on growth in exports of goods while exports of services remained virtually unchanged.

In 2017 the volume of exports will increase by a couple of per cent. Exports of goods will grow by 2.5 per cent and exports of services by over one per cent. Exports are driven by the gradual recovery of investment activity in the export markets, improved competitiveness as a result of the competitiveness agreement and capacity increasing as a result of investment. Motor vehicle industry exports will increase by as much as 32 per cent as a result of the significant expansion of the Uusikaupunki car plant and increased ship exports. Timber industry exports will increase by 6 per cent. Metal refinement and electronics exports will increase 2-3 per cent. Paper industry exports will grow by one per cent. Exports to Russia will already see a small increase.

In 2018 the total volume of exports is forecast to grow by 2.5 per cent. Exports will increase on a broad front in a number of industries. Paper industry exports will increase very rapidly as a result of new capacity in the Äänekoski bioproduct mill. Exports to Russia and other raw material producing countries will strengthen if commodity prices rise as expected. In 2019 the volume of exports will increase by over three per cent, supported by large ship deliveries. It is important for the development of exports in the next few years that wage settlements are moderate. Finland’s cost competitiveness is not yet at a sufficient level, and therefore unit labour costs should rise less than in competing countries for several years.

Investment increased last year by 5.2 per cent compared to the previous year. Private investment increased by 6.3 and public investment by 0.7 per cent. Residential housing construction grew by almost 12 per cent. According to Statistics Finland, 80.1 per cent of industrial production capacity was in use in December of 2016, which was 1.9 percentage points more than the previous year.

Investment is forecast to grow by almost 4 per cent in 2017. Machinery and equipment investment will increase by 6 per cent. Residential housing construction investment growth will slow down to 4 per cent. Public investment will also show pronounced growth due to major infrastructure projects.

In 2018 total investment will increase by 2.5 per cent. Machinery and equipment investments will increase a couple of per cent. Residential housing construction growth will remain moderate at about three per cent. Housing demand will remain high in growth centres. In 2019 overall investment growth will rise to about three per cent, as the growth of enterprises’ machinery and equipment investment is boosted by nuclear power plant investment.

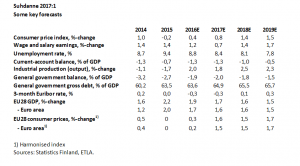

Recently strengthened domestic demand has also bolstered employment, which has improved in construction in particular. In 2016, the unemployment rate was 8.8 per cent, which was 0.6 percentage points lower than the previous year. For 2017 we forecast an 8.4 per cent unemployment rate and 69.2 per cent employment rate. In the following years the unemployment rate will fall by 0.3 percentage points per year. It will be 8.1 per cent in 2018 and 7.8 per cent in 2019. The improvement in exports will also foster employment in the industrial sector. In the year 2021 we expect the unemployment rate to be 7.3 per cent and the employment rate to be 71 per cent.

In 2016 low inflation and the improving employment situation increased the disposable income of households. Private consumption grew by 2 per cent. It was also partly sped up by strong household confidence, which spurred a decline in the savings rate into negative territory.

In 2017 the moderate wage settlements, increased labour-related costs paid by the employee due to the competitiveness agreement, public holiday pay cuts and accelerating inflation will together keep real earnings at last year’s level. However, the improving employment situation and household confidence will spawn 1.3 per cent growth in private consumption.

In 2018 private consumption will increase by 1.1 per cent. Real disposable household income will grow by over one per cent in the wake of higher employment and non-labour income growth, even though we have assumed that real earnings will remain virtually unchanged considering the moderate wage increases. In 2019 private consumption will grow by 1.2 per cent, which represents an increase approximately equal to the rise in real disposable income coming from the improvement of employment. We estimate that real income will also rise somewhat at this point. If wage agreements are not moderate, consumption growth might be faster in the short term, but declining employment will limit GDP growth and consumption in the long term.

In 2016 consumer prices increased by 0.4 per cent from the previous year. International inflation accelerated slightly as a result of oil price increases. In 2017 consumer prices are estimated to increase by 0.8 per cent. Inflation is still fuelled by the rise of oil prices. In 2018 consumer prices are estimated to increase by 1.4 prices as the moderate ascent of oil prices continues. In 2019 consumer prices will rise by 1.5 per cent. At this point, the rising interest rate level will contribute to higher inflation.

In 2016 the total public sector deficit was 2 per cent relative to GDP in our forecast. The central government deficit was 2.6 per cent while the municipalities’ deficit was 0.4 per cent relative to GDP. The surplus of social security funds was one per cent. According to our estimates, the so-called structural deficit of the public sector was 0.8 percent in proportion to GDP. The EMU norm is a maximum of 0.5 per cent, but it has its own flexible mechanisms. The general government gross debt stood at 63.3 per cent relative to GDP according to our estimates, which was approximately the same as the previous year. Debt growth was held back by the simultaneous reduction of the central government cash funds.

In 2017 the public sector deficit will remain at roughly last year’s level. The narrowing of the deficit will temporarily come to a halt due to income tax cuts implemented for the current year. The public debt will rise to 64.9 per cent relative to GDP. The public sector’s structural deficit, calculated on the basis of ETLA’s forecast using the EU Commission’s methodology, will be 1.4 per cent relative to GDP in 2017.

In 2018, the public sector deficit will fall to 1.8 per cent as the central government deficit shrinks thanks to cost-cutting and economic growth. The surplus of social security funds will decrease gradually as pension expenditures increase. The public sector structural deficit will be 1.4 per cent of GDP, the same as the previous year. The public sector’s gross debt will reach 65.5 per cent of GDP.

In 2019 the deficit of the total public sector will continue to decline to 1.5 per cent in relation to GDP. The central government deficit will be 1.9 per cent of GDP at that point.

Finland clearly meets the 3 per cent target for the public sector deficit. In 2021 the deficit will be about one per cent of GDP. However, the deficit constitutes a problem because it increases the debt. Public debt is increasing in relation to GDP in the coming years, reaching its peak in 2019. In 2020 it will already start to fall. The decline will continue in 2021 when the public debt is 65 per cent of GDP, which is roughly the same as in the current year. As the level of debt compared to other EMU countries is low, it is probably acceptable assuming that the debt is decreasing. This development is nevertheless very sensitive with respect to economic growth.

The structural deficit will be Finland’s biggest problem with respect to the so-called “preventive arm” of the EMU criteria in the next few years. It is calculated by making cyclical and structural adjustments to the public sector’s actual deficit. The essential question in the calculation is how large is Finland’s potential output estimated to be. The greater the output gap between the potential and actual GDP, the lower the structural deficit in relation to the actual deficit. When the output gap shrinks, the structural and the actual deficit converge. According to our estimates, the structural deficit will exceed the EMU norm in 2017 and 2018.

The EMU criteria includes an additional criteria called the expenditure rule. It specifies that public spending should not grow faster than potential GDP. Again, according to this criterion, Finland may break the rules.

If different criteria point in different directions, the assessment can utilize wide discretion. The Commission will nevertheless in any case closely monitor the development of our country’s public finances and make policy recommendations.

Further information:

Markku Kotilainen

Research Director, Dr. Soc. Sc. (Econ.)

ETLA-Research Institute of the Finnish Economy

tel. +358-9-609 90 206

email:markku.kotilainen@etla.fi