FINNISH ECONOMY 2018/1

Finland’s economic growth continues to be robust. GDP will increase by 2.8 per cent in 2018, bypassing the level of output prevailing in 2008. GDP will grow by 2.4 per cent in 2019 and by 1.9 per cent in 2020. GDP growth will be faster in the next few years than growth of potential output, which is estimated to be about 1.5 per cent.

The favourable economic development is driven by the strong performance of the global economy, which Finland will be able to exploit due to its improved competitiveness.

Finland’s export markets will continue to grow swiftly, albeit at a slightly decelerating rate. Investment activity, which is important for exports, will also pick up considerably. The greatest risks are related to the financial markets, international politics and trade liberalization.

The volume of exports will increase by 4 per cent in 2018, driven by stronger demand, improved competitiveness and greater capacity. The rate of growth will subside to slightly above 3.5 per cent in 2019 and to 2.5 per cent in 2020.

Private consumption will climb by a couple of per cent in 2018. The rise in the level of earnings and an upturn in employment will boost the purchasing power of households. In 2019-2020 the acceleration of inflation will dampen the rate of consumption growth to 1.6-1.7 per cent.

Growth in investment will slow down to 3 per cent in 2018 after the completion of numerous large projects. In 2019 growth will accelerate to around 4.5 per cent.

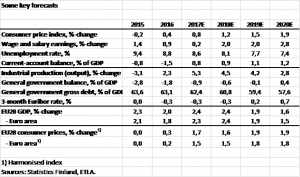

The unemployment rate will fall to 8.1 per cent in 2018. Thereafter it will fall to 7.7 per cent in 2019 and to 7.4 per cent in 2020. By 2022 it will reach 6.9 per cent, provided that the mismatches between the supply and demand of labour diminish.

Finland’s consumer prices will rise by 1.2 per cent this year, 1.5 per cent in 2019 and 1.9 per cent in 2020.

Public finances will be approximately in balance in 2019, perhaps already in 2018.

The global economy is in the midst of an upswing. GDP is estimated to grow in the US by 2.6 per cent in 2018 and by a couple of per cent during 2019-2020. The growth will be driven by domestic demand, which will be bolstered by fiscal policy in the coming years. The growth rate will be slightly faster than the growth of potential output, leading to an acceleration of inflation and a rise in interest rates. President Trump’s policies are a major source of uncertainty, especially regarding fiscal and trade policies.

GDP growth in the total EU area will be 2.4 per cent this year, 1.9 per cent in 2019 and 1.6 per cent in 2020. This year’s growth has been clearly faster than expected, although the anticipation of Brexit is holding back Britain’s growth. In Europe, growth is also faster than potential output growth. High unemployment will nevertheless dampen the acceleration of inflation. In Russia, GDP will expand by a couple of per cent in 2018 and by around 1.5 per cent annually in 2019-2020 as energy prices become more stable. In the longer term, an increase in the rate of economic growth will require the acceleration of reforms. China’s GDP will climb by 6.6 per cent this year, which is more than forecast last spring. Efforts to curb the indebtedness of the rapidly expanding private sector and the shift from export-driven industries to services will dampen production growth over the next few years. In 2019 growth will slow down to 6.3 per cent and approach 6 per cent next year.

In 2018 the gross world product will expand by 3.8 per cent, i.e. the same as last year. In 2019 growth will slow down slightly to 3.5 per cent. At this point, growth in emerging economies will be curbed by the slowdown in China’s growth. Countries producing raw materials will benefit from the moderate rise in commodity prices over the next few years.

The risk of a slower rate of growth than forecast still exists. Monetary policy is being tightened in the US and will soon also be tightened in the euro area. This creates a potential risk for the financial markets and thus also for the real economy. As the level of public debt in many euro area countries is high and banks’ capital adequacy is rather weak, the economies of the euro area are also susceptible to disturbances. In China, the biggest problem is the high level of debt in the business sector, which may under conditions of weak economic development spur difficulties in debt servicing. There are also still concerns about the protectionist policies of President Trump. Recently, even the threat of a trade war has started to look plausible.

Eastern Ukraine is bogged down in a frozen conflict. Old Russian sanctions will not be lifted in the near future and new ones will be introduced. The political crisis will hamper economic relations between Russia and Western countries for several years. Uncertainty is also being spawned by the war still going on in Syria and Iraq as well as threats relating to North Korea’s nuclear proliferation and potential countermeasures.

According to recent estimates, in 2017 GDP in the euro area grew by 2.3 per cent, which was significantly higher than forecast in the beginning of last year.[1] Total GDP growth in the region grew by a steady 0.6-0.7 per cent last year on a quarterly basis. Leading indicators suggest that this positive trend has continued in the first quarter of this year. Future growth will be essentially dependent on developments in business and household confidence. Low interest rates are boosting the growth of euro economies. The appreciation of the euro will dampen the export performance of these countries somewhat.

We forecast that euro area GDP will grow by 2.4 per cent in 2018 and by 1.9 per cent in 2018. Growth will slow down to 1.5 per cent in 2020.

There will also be differences in growth rates between euro economies during the next few years. In 2018 GDP growth in Ireland will be 4.5 per cent, in the Netherlands 3 per cent, in Germany, Spain and Greece 2.5 per cent, in France 2 per cent and in Italy about 1.5 per cent. The current accounts will be strengthening and the rise in the public debt will slow down. A large public debt still makes the economies of many euro countries vulnerable.

The monetary policy of the euro area is very loose and it is normalizing slowly. We estimate that the ECB will discontinue its securities purchases at the end of 2018, but raising the key interest rate will have to wait until the second half of 2019.

A direct consequence of the ECB’s loose monetary policy is that interest rates will remain low and the exchange rate of the euro will be weaker than otherwise would be the case. Low interest rates and strong liquidity will bolster share prices. In some countries, the loose monetary policy may bring about an unhealthy rise in housing prices.

The strengthening the euro area crisis management mechanisms has, together with the ECB’s loose monetary policy and robust economic growth, calmed the region’s financial markets. The risk of crises still exists, however, as the public debt is high in many countries and there are several banks with low solvency in the region (especially in Italy). The threat of a new crisis in Greece also exists.

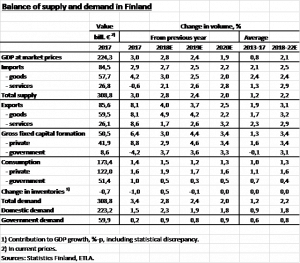

According to preliminary data from the National Accounts, Finland’s GDP grew by 3.0 per cent in 2017 compared to the previous year. The volume of total exports rose by 8.3 per cent. Exports increased significantly in several geographic areas, including Russia. Private consumption increased by 1.6 per cent. Consumption was spawned by low inflation, the improvement of employment, a rise in non-wage income and strong consumer confidence. Investment climbed by 6.3 per cent.

GDP will GRoW by 2.8 per cent in 2018, 2.4 per cent in 2019 and 1.9 per cent in 2020

We project that Finland’s GDP will increase by 2.8 per cent in 2018. In September, we forecast growth of 2.0 per cent. This revision is mainly due to stronger growth in the international economy, which is reflected in improved export prospects. This year exports will grow by 4 per cent. Investment will rise significantly less than last year as many major investment projects have been completed. Private consumption will grow by a couple of per cent, spurred by improved employment, rising real earnings and a low savings rate. In 2019 GDP will grow by 2.4 per cent. Growth in exports will slow down due to the slackening of demand. Investment growth will accelerate slightly. Private consumption will grow slightly less than during this year. In 2020 GDP will expand by 1.9 per cent, which is still somewhat swifter than the growth of potential output. Growth will be fuelled by exports and investment in particular.

In 2018 the volume of exports will increase by 4 per cent. Exports of goods will climb by about 5 per cent. Growth in exports of services will slow down to about 1.5 per cent after the strong growth of last year. Exports are boosted by the rapid growth in investment activity in export countries, the improvement in competitiveness due to the Competitiveness Pact and the expansion of export industry capacity in the wake of investment. Paper industry exports will grow by over 4 per cent. Pulp exports will experience particularly rapid growth spurred by the new capacity of the Äänekoski biotech plant. Exports of timber products will increase by 5 per cent due to the high level of construction in export markets. Exports of motor vehicles will jump by about 50 per cent due to the sizable expansion of the Uusikaupunki car plant. Exports of other transport equipment (mainly ships) will drop by more than a fifth from last year. Exports of machinery and equipment as well as metal products will be up by 3.5 per cent over last year. Exports of the electronics industry will expand by 5 per cent, but exports of other electrical equipment will remain at last year’s level. The growth of exports is occurring across a wide geographical area.

In 2019 the volume of total exports is projected to increase by about 3.5 per cent. Growth will slow down from that prevailing this year as the growth of the export market subsides. The amount of ships delivered, however, will be up significantly from this year. In 2020 export growth will slow down to 2.5 per cent, as international demand slackens moderately. The fairly positive export performance projected is based on the fact that cost competitiveness will continue to improve slightly in the next few years. This will require continuing wage restraint even after the current wage agreement expires.

We forecast that investment will increase by 3 per cent in 2018 after last year’s growth of 7.4 per cent. The growth is curbed by the completion of some major projects last year. Machinery and equipment investment will remain at last year’s level due to the high level of comparison. Growth in residential construction investment will continue to grow rapidly at just under 4.5 per cent. Public investment will experience growth of about 3.5 per cent.

In 2019 total investment growth will accelerate to nearly 4.5 per cent. Machinery and equipment investment will grow by 5.5 per cent due to rising capacity demand. Growth in residential construction will continue at an almost 4 per cent pace spawned by migration. In 2020 growth in overall investment will decelerate to about 3.5 per cent as a result of the slowdown in global economic growth.

The recent strengthening of economic growth has also boosted employment. The number of employed persons has increased by 63,000 from January of 2015 to January 2018 and the seasonally adjusted employment rate has increased by 2.6 percentage points to 70.9 per cent. We forecast that this development will continue. Employment will increase by about 100,000 people from 2015 to 2019. The employment rate will rise to 71.6 per cent. The government’s goal of 110,000 new jobs and a 72 per cent employment rate is thus close to being achieved. The unemployment rate will also decline, but less than could be expected merely based on employment developments, as the supply of labour is also increasing. For 2018, we forecast an unemployment rate of 8.1 per cent. Thereafter, the unemployment rate will decrease to 7.7 per cent in 2019 and to 7.4 per cent in 2020. Employment in industry will be boosted by the pick-up of exports but dampened by the rise in productivity. We estimate that the unemployment rate will be 6.9 per cent in 2022 with an employment rate of 73 per cent. This development requires that mismatches between the supply and demand of labour diminish and that wage pressures remain under control.

In 2018 improving employment, rising real earnings and other income, as well as strong household confidence, will lead to around 2 per cent private consumption growth. The savings rate will remain clearly negative.

In 2019 private consumption will increase by 1.7 per cent. The real disposable income of households will grow by the same amount, fuelled by improving employment and income growth. We have projected a rise in real income of 0.5 per cent.

In 2020 private consumption will grow by 1.6 per cent, which is equivalent to the increase of real household disposable income. If wage hikes exceed our forecast, the growth in consumption may be faster in the short term, but a long-term decline in employment would limit GDP growth and consumption growth.

In 2018 consumer prices are expected to rise by 1.2 per cent. Inflation is accelerated by the upswing in oil prices from last year’s level and also the rise in food and alcohol prices. In 2019 consumer price increases are projected to accelerate to 1.5 per cent as a result of an upswing in housing prices and other services. Consumer prices will climb by 1.9 per cent in 2020, when rising interest rates contribute to the acceleration of inflation somewhat.

Public finances are anticipated to be in balance faster than previously forecast due to strong economic growth. In 2017 the total public sector deficit was 0.9 per cent of GDP according to our estimate. The central government’s deficit was 1.8 per cent while that of the municipalities was 0.1 per cent. The surplus of social security funds was one per cent. In the public sector, we estimated that the so-called structural deficit was 0.6 per cent in relation to GDP. The corresponding EMU norm is a maximum of 0.5 per cent, but it has its own adjustment mechanisms. The gross debt for the general government was 62.4 per cent of GDP, which was just slightly less than one percentage point lower than in the previous year.

In 2018 the public sector deficit will subside to 0.6 per cent of GDP in the wake of rapid economic growth. The government deficit is projected to be 1.5 per cent of GDP. The surplus of social security funds will fall to 0.9 per cent as pension expenditure increases. The public debt will decline to 60.8 per cent of GDP. Using the methodology of the EU Commission and calculated on the basis of Etla’s forecast, the public sector structural deficit is projected to remain at last year’s 0.6 per cent of GDP due to the narrowing of the so-called output gap.

In 2019 the deficit of the public economy will shrink almost completely to 0.1 per cent of GDP, as the central government deficit decreases to less than 1 per cent of GDP due to economic stimulus and economic growth. The surplus of social security funds will remain at 0.9 per cent. The public sector structural deficit will be 0.8 per cent of GDP. The deficit will be decreased by a decline in the actual deficit, but the output gap becoming positive will have the opposite effect. The ratio of public debt to GDP will fall to 59.4 per cent.

In 2020 the total public sector will start to run a surplus of 0.4 per cent of GDP. At this point the central government deficit will be 0.3 per cent of GDP. The ratio of public debt to GDP will fall to 57.7 per cent of GDP. Keeping a tight rein on public sector spending and earnings is a prerequisite for the favourable development. Central government finances will stabilize in 2021.

Finland clearly complies with the 3 per cent criterion for the public sector deficit. The pick-up in economic growth has also significantly eased the fulfilment of the 60 per cent debt criterion. The debt will not climb as high as previously estimated and in 2019 the debt-to-GDP ratio will already fall below the 60 per cent ceiling. The fall will continue so that in 2022 the debt will be 53.8 per cent of GDP. The trend is nevertheless very sensitive to economic growth and the GDP deflator.

With regards to the so-called preventive arm of the EMU criterion, the structural deficit is still a problem for Finland. It is calculated from the actual public sector deficit by making cyclical and structural adjustments. The key question in the calculations is how high the so-called potential output of Finland is estimated to be. The higher the difference between the potential GDP and the real GDP (negative output gap), the smaller the structural deficit is relative to the actual deficit. As the output gap closes, the structural and actual deficits are equal. We estimate that the structural deficit will exceed the medium-term target level in 2018 and 2019. However, since the deficit will remain below 1 per cent (the difference is not significant) and will not be increasing appreciably, the structural deficit criterion will also be met.

The EMU criteria still have additional conditions for so-called spending rules. This means that public spending growth should not be faster than potential GDP growth. The interpretation of this measure is still evolving. The difficulties with this indicator pertain to the uncertainties regarding the calculation of potential output.

[1] For more information, see Etla’s recent study on forecast errors https://www.etla.fi/julkaisut/etlan-suhdanne-ennusteiden-ennustevirheet-vuosina-2014-2017/

Further information:

Markku Kotilainen

Research Director, Dr. Soc. Sc. (Econ.)

ETLA-Research Institute of the Finnish Economy

tel. +358-9-609 90 206

email:markku.kotilainen@etla.fi