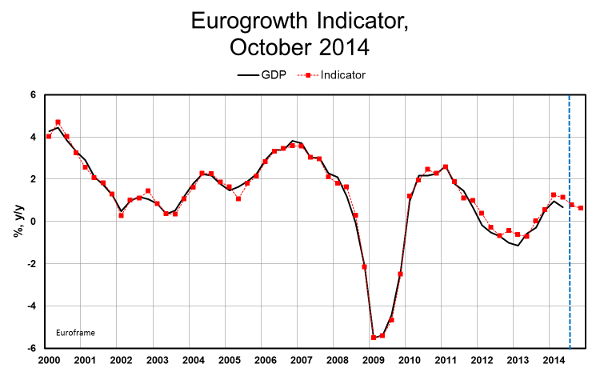

Euro Area growth remains weak at 0.2 and 0.1 per cent in the third and fourth quarters of 2014 according to the Eurogrowth Indicator calculated by the Euroframe group in October. The quarterly growth estimates translate to 0.8 and 0.6 percent year-on-year growth rates, respectively.

The growth estimates were unchanged from September, although the model was re-estimated. However, the composition of the growth contributions changed somewhat due to the new estimation. The independent variables were the same as in the previous model, but the lead of construction survey was extended by one quarter to five quarters and two lags of the dependent variable were added.

While re-estimation improved statistical properties of the model, its message continues to be quite bleak. The quarterly contributions from the industrial survey improved slightly from September, but confirm a worsening of the previously robust industrial sentiment since the beginning of the year. The contribution of the construction sentiment with a long lead weakened a bit and continues as a drag to the growth.

The impact of household survey to the quarterly GDP estimates changed quite much in the October estimation. Historical contributions were in general much better and the estimates of the third and fourth quarters turned positive from their previous negative impacts.

The real USD/euro rate has a neutral impact on the two quarterly GDP estimates. The recent devaluation of the euro vis-à-vis the USD due to a change in interest rate outlooks in the US and in the Euro Area will affect the indicator with a lag in early 2015.

The weakening of the euro after the ECB’s related announcements on reductions in its key rates and on new unconventional monetary policy measures in September should support the weakening industrial confidence. However, the uncertainty relating to the crisis in Ukraine seems to be very persistent and unpredictable. The crisis has obviously already weighed negatively in particular on the Euro Area industrial confidence and turned its contribution negative since the second quarter of 2014. Should the crisis flare up again, it would weaken the estimate of the fourth quarter GDP growth in the Euro Area further.

6.10.2014

Paavo Suni